What Foreign Buyers Really Need to Know

Two taxes tend to cause the most confusion for foreign buyers of real estate in Costa Rica: the capital gains tax and the luxury home tax. Neither is especially complicated, but both are often misunderstood, particularly by buyers coming from countries with very different tax systems. This overview focuses on the points that matter most in real-world transactions, without getting overly technical or legalistic.

Capital Gains Tax

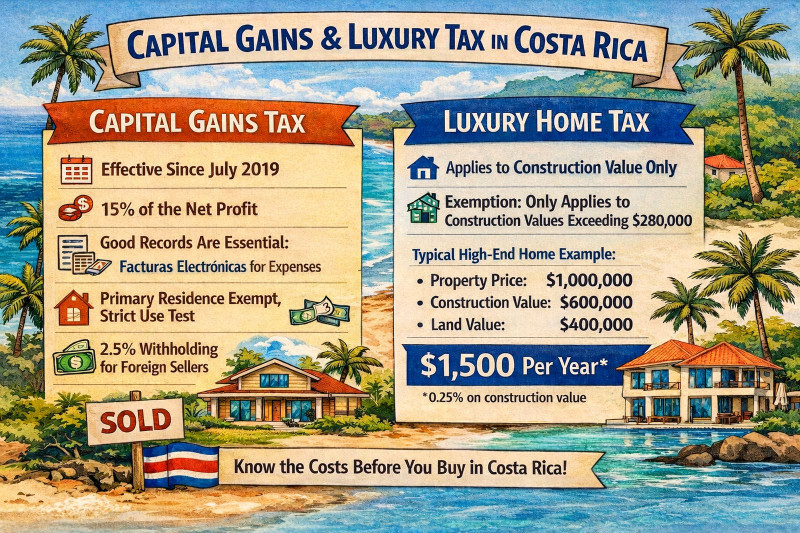

Costa Rica’s capital gains tax was enacted in July of 2019. For properties acquired after the law went into effect, the tax is assessed at 15 percent of the net gain when the property is sold. In simple terms, this is the difference between what you paid for the property and what you sell it for, after accounting for allowable costs.

There is a transitional rule for properties owned prior to the enactment of the law, allowing sellers to choose a flat 2.25 percent tax on the gross sales price instead of the 15 percent capital gains tax. While this option can still be relevant for long-time owners, it is generally not a significant factor for current buyers, since most new purchases fall squarely under the standard capital gains regime.

For today’s buyers, the most important issue is documentation. Capital gains tax is calculated based on your documented cost basis, so good recordkeeping is essential. This includes not only the purchase price but also qualifying improvements and transaction costs. In Costa Rica, this means proper invoices, ideally facturas electrónicas, for construction, renovations, professional fees, and other eligible expenses. Without solid documentation, it can be difficult to justify a higher basis, which may result in paying more tax than necessary when you eventually sell.

There is an exemption for a primary residence, but it is applied strictly. The exemption is based on actual use of the property as your principal home, not simply ownership or immigration status. Authorities look at how much time you have actually spent living on the property and whether that use is consistent with your declared domicile in Costa Rica. This approach aligns more closely with the concept of domiciliation than with legal residency alone. Vacation homes or properties used primarily as rentals generally do not qualify for this exemption.

Foreign sellers should also be aware of the mandatory withholding at closing. When a foreigner sells Costa Rican real estate, the buyer is required to withhold 2.5 percent of the gross sales price and remit it to the tax authorities. This amount is credited against any capital gains tax ultimately owed and can later be reconciled, but it does affect cash flow at closing.

Luxury Tax

The luxury home tax is a separate, annual tax that applies only to residential properties whose construction value exceeds a minimum threshold. One of the most important points to understand is that this tax applies only to the declared value of the building itself. The land value is excluded entirely from the luxury tax calculation.

For the current tax period, the exemption threshold is approximately 143 million colones, which is roughly $280,000 US depending on the exchange rate. If the declared construction value is below that amount, no luxury tax is owed. If it exceeds the threshold, the construction value is taxed using a progressive rate schedule. Crossing the threshold does not cause the tax to apply to the entire property value, and it never applies to the land.

A concrete example helps clarify how this works in practice. Assume a property is purchased for $1,000,000. The declared construction value is $600,000 and the declared land value is $400,000. For luxury tax purposes, only the $600,000 construction value is relevant. The $400,000 land value is excluded entirely.

Because the construction value exceeds the approximate $280,000 threshold, the property is subject to the luxury home tax. Under the current brackets, a construction value at this level generally falls within the lowest luxury tax rate of approximately 0.25 percent. Applied to this example, the annual luxury tax would be about $1,500 per year ($600,000 multiplied by 0.25 percent). This tax is assessed annually and is paid in addition to the standard municipal property tax, which is roughly 0.25 percent of the registered value.

As a practical rule of thumb, for homes priced around one million dollars, the luxury tax often feels like it roughly doubles the annual property tax burden, increasing it from about 0.25 percent to something closer to 0.5 percent. This is not an exact doubling, since the standard municipal property tax of approximately 0.25 percent is applied to the total registered value of the property (land plus construction), while the luxury tax of approximately 0.25 percent is applied only to the construction value once the threshold is exceeded. Still, thinking of the combined impact as “roughly half a percent per year” provides a quick, back-of-the-napkin way for buyers to estimate the luxury tax effect without getting lost in the details.

For foreign buyers, the takeaway is that both taxes are manageable with proper planning. Capital gains tax is largely about documentation and understanding how use of the property affects exemptions. The luxury tax is about understanding how construction value is declared and whether it exceeds the applicable threshold. Neither should be an afterthought, but neither is typically a deal breaker when properly understood.

As with many aspects of real estate in Costa Rica, clarity up front and realistic expectations go a long way toward avoiding surprises later.